From paper to algorithms, from employee to smart machine, the mortgage industry is undergoing a paradigm shift as artificial intelligence enters the loan application process. Does this open the door to an era of transparency and efficiency? Or does it raise concerns about privacy and hidden biases?

Mortgage appraisal: From traditional processes to smart transformation

<In the traditional system, banks and real estate finance companies rely on human analysts to screen loan applications, review financial documents, assess property value, and study the borrower's creditworthiness.But this process is time-consuming, subject to individual judgment, and can be influenced by subjective factors.

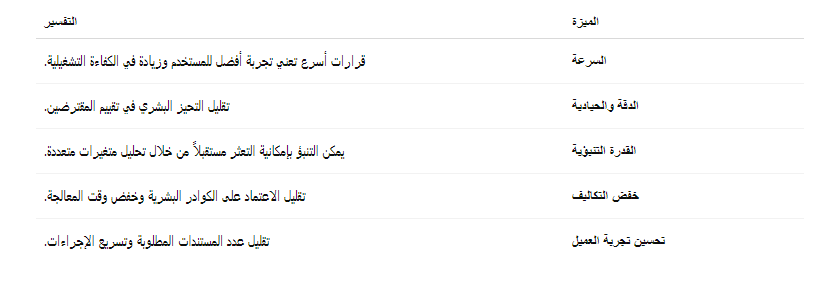

This is where AI comes in. Artificial intelligence (AI) is reshaping the landscape, with big data analytics models and machine learning algorithms that can make accurate decisions very quickly.

.

How is AI used to evaluate real estate loans?

Analyzing a borrower's creditworthiness Algorithms use financial and non-financial data, such as credit history, income level, monthly obligations, and even spending behaviors.

They can detect indicators of default or repayment ability that are not readily apparent in traditional models. Accurately estimate the value of a property.

<Accurately estimate the value of a property Image analysis techniques are used to review photos of the property and verify its actual condition.

Speed up procedures and approvals Fraud detection Despite the advantages, the use of AI is not without its challenges: Algorithm bias

Algorithm bias

If models are trained on biased historical data, decisions may continue to repeat past mistakes, such as discrimination against certain groups. Lack of transparency

Lack of transparency Privacy and data protection

<Relying on large amounts of sensitive data raises questions about protecting users“ privacy.

Excessive reliance on automation

<In exceptional or complex cases, algorithms may fail to read human context or personal circumstances.

Global banks like JPMorgan and HSBC are already using AI systems to analyze loans and assess risk. Global banks like JPMorgan and HSBC are already using AI systems to analyze loans and assess risk.

Financial technology (FinTech) companies like Blend and Zest AI are offering smart solutions to traditional banks in the area of evaluating real estate loans. In the Arab region, some banks are already using artificial intelligence systems to analyze loans and assess risk.

In the Arab region, some banks in the UAE and Saudi Arabia have started testing AI solutions within credit models. In the Arab region, some banks in the UAE and Saudi Arabia have started testing AI solutions within credit models.

Advantages of adopting AI in real estate finance

Challenges and Concerns

Examples of AI adoption in real estate finance

Is AI a replacement or complement?

<According to experts, artificial intelligence does not completely eliminate the role of humans, but rather complements it.

While the machine handles repetitive analytical tasks, the human element still has an important role in final review, dealing with exceptional cases, and communicating with clients.

.

With increasing demand for real estate loans in emerging markets and a growing need to make accurate and fast financial decisions, artificial intelligence is an indispensable tool for the near future. With the right controls in place, artificial intelligence (AI) is an indispensable tool for the near future.

With ethical controls and data protection, this technology can strike a balance between innovation and efficiency, fairness and transparency, and open the door to more inclusive and equitable financing opportunities. With the increasing demand for real estate loans in emerging markets and the growing need for accurate and fast financial decisions, AI is an indispensable tool for the near future.

Smarter, more transparent finance