In an unprecedented demographic and social shift, Saudi society is witnessing a remarkable rise in the phenomenon of “solo living” among young men and women. For the first time in the Kingdom's history, a growing number of young people are moving towards residential independence before marriage, driven by profound economic and social changes.

This radical shift is not only affecting the social structure, but also reshaping the entire real estate demand, creating untapped investment opportunities in a market that is still largely focused on building “extended family villas”.

The question arises: Who is building for the new Saudi bachelor generation?

Demographic Shift: The Numbers Speak

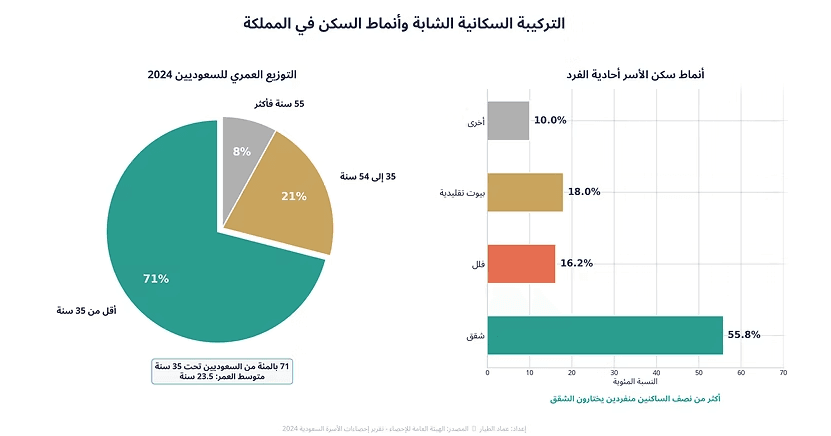

To understand the magnitude of this shift, one must first look at the Kingdom's young demographics. According to the General Authority for Statistics report for 2024, young people under the age of 35 make up 71% of the total Saudi population, with an average age of just 23.5 years. This huge demographic is entering the labor market and making their housing decisions with increasing independence, in a very different landscape from what their parents" generation knew.

The 2024 Saudi household statistics indicate that single-person households have become a significant segment of the housing ecosystem. Interestingly, 55.8% of these households live in apartments, while only 16.2% live in villas. This decisive trend towards apartments reflects a fundamental change in the lifestyle and purchasing power of this segment.

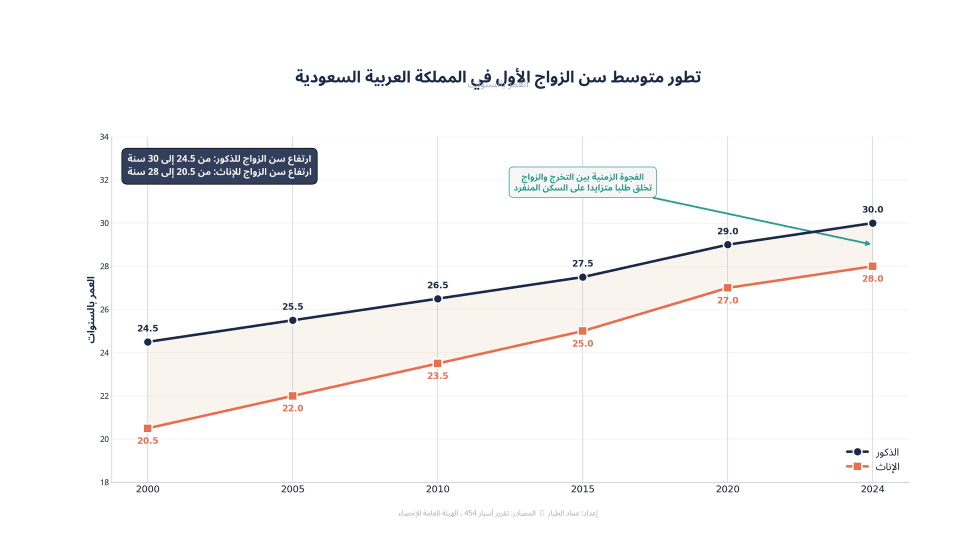

Parallel to this, society is witnessing a significant delay in the age of marriage. The average age of first marriage has risen to 28 for women and 30 for men, compared to 20.5 and 24.5, respectively, at the turn of the millennium. A recent academic study reveals that the rate of reluctance to marry among Saudi youth has reached 46.8%, a historically unprecedented rate.

65.3% of Saudi youth are currently unmarried, and the proportion of married people in the total population decreased from 54.09% in 2024 to 52.This delay, whether by personal choice or as a result of real economic pressures (with the cost of a wedding in major cities ranging from 145,000 to 850,000 riyals, with a rise of 30% in 2023 alone), creates a years-long time gap between graduating from university and starting a family. This gap is precisely the period in which the rising demand for single-family housing emerges.

To illustrate the magnitude of the economic challenge, it is enough to know that the salaries of young people range between 4,000 and 7,000 riyals per month, while rents have increased by 9.7% in 2025. This difficult equation makes individual housing in small, affordable units a necessity, not an option.

Gap between supply and demand: Who is building for the singles generation? Historically, the Saudi real estate market has been designed to cater to the needs of the extended or large family.

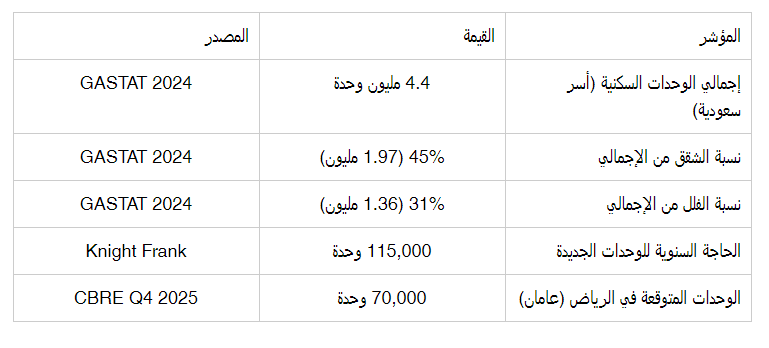

According to GASTAT data for 2024, the total housing units occupied by Saudi households totaled 4.4 million units, a growth of 2.7% (233,000 new units). Although apartments make up 45% of this total (1.97 million apartments), most of these apartments are designed with large spaces (3 to 4 bedrooms) to suit families, not independent individuals. Most of these apartments are designed with large spaces (3 to 4 bedrooms) to suit families, rather than independent individuals.

Herein lies the real investment gap: Demand for studio and one-bedroom apartments in central locations close to work and entertainment areas is growing, while supply remains scarce. Young freelancers are looking for compact, easy-to-maintain, low operating cost spaces, favoring strategic location over large space.

Knight Frank data confirms that the Kingdom needs to build 115,000 housing units per year until 2030 to meet growing demand, totaling 825,000 units over the 2024-2030 period. The pivotal question: How many of these units will be designed to meet the needs of a single occupant?

Investment Returns: Why is the studio the winning horse? This superiority is due to three fundamental reasons.

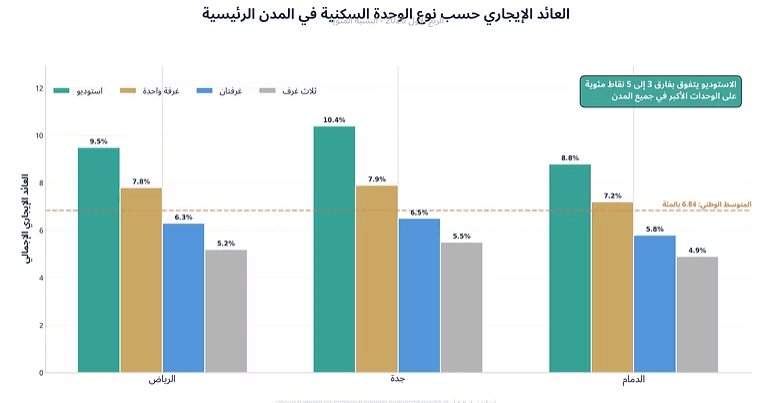

Studio apartments achieve the highest rental yield in all major cities, outperforming three-room units by 3 to 5 percentage points (9,10) Studio apartments achieve the highest rental yield in all major cities

In a broader context, the market for ownership apartments in major cities is undergoing a remarkable transformation. Prices range from SR500,000 to SR1 million, with market experts emphasizing that "central locations give small apartments a higher value than large units in outlying areas." Figure

Foreign Professionals: The hidden driver of demand for single-family housing White-collar expats are a key segment that is reshaping the rental market in major cities.

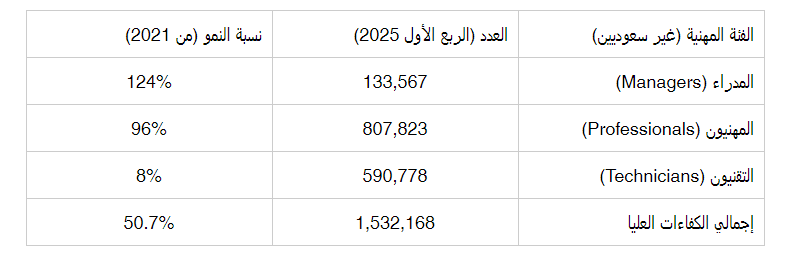

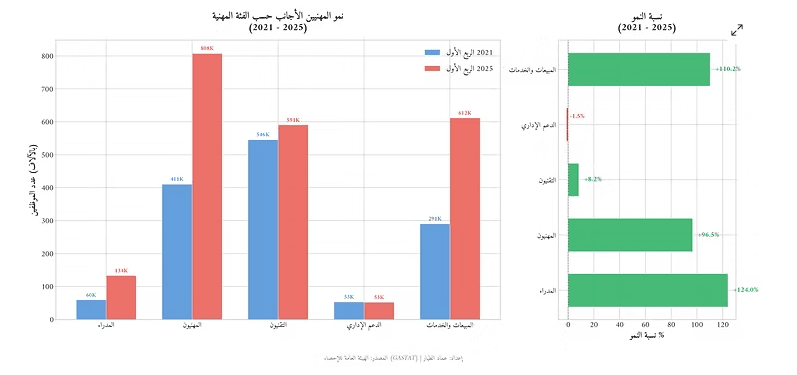

According to GASTAT data for the first quarter of 2025, the number of foreign professionals in higher categories (managers, professionals, and technicians) reached more than 1.53 million employees, registering an exceptional growth of 50.7% compared to 2021. If we add the administrative and sales support categories, the total of this segment is close to 2.2 million employees.

These talents, which the Kingdom is attracting as part of the Vision 2030 targets in the technology, tourism, renewable energy, and finance sectors, are often on individual employment contracts. A recent Mercer study reveals that 75% of companies in Saudi Arabia offer a separate housing allowance to their employees, and these allowances increased by 8% between 2024 and 2025 to keep pace with rising rents.

These figures confirm that the demand for single-family housing is not only driven by Saudi youth, but also by foreign buyers looking for compact, modern, and close to business centers, making investment in this sector a strategic choice with double returns. These figures confirm that the demand for single-family housing is not only driven by Saudi youth, but also by foreign buyers looking for compact, modern, and close to business centers.

A global phenomenon with a Saudi flavor: An International Comparison

In Scandinavia, the proportion of single-person households exceeds 40%. In Japan, this proportion has risen by 50% over the past two decades, leading to a radical shift in the real estate market towards compact units and the concept of "smart living." Saudi Arabia is at the beginning of this wave.

Long-term demographic and economic impacts

1- The first is neighborhood redesign. We will see an accelerated shift towards "mixed-use" developments that integrate compact housing with Co-working spaces, cafes, and essential services, to cater to the fast-paced lifestyle needs of young, independent people. This model is already emerging in Vision 2030 megaprojects and is expected to expand to existing neighborhoods.

2- The second theme is changing consumption patterns. Single-person households have fundamentally different consumption patterns than traditional households. This segment leans more towards services, food delivery, out-of-home entertainment, and digital subscriptions, which will stimulate new economic sectors and redistribute consumer spending.

3- The third theme relates to fertility rates. The delayed age of marriage and residential independence are globally associated with declining fertility rates, which have already declined in the Kingdom from 6.6 in 1960 to 2.28 in 2023, with expectations of reaching 2.12 in 2025. This decline, while natural in the context of the demographic transition, calls for smart urban and economic policies that support future family formation without losing sight of the needs of the growing segment of single residents.

Conclusion: An opportunity for those who read the shifts The market needs 115,000 housing units per year until 2030 to meet demand. The winners at this stage will be those who realize that the new "singles generation" is not looking for vast spaces, but quality of life, central location, and smart design. Investing in studios and small apartments is not just a response to a current demand, but a bet based on an accurate reading of the future demographics of the Kingdom.

The opportunity is clear for developers and investors who have the courage to read and respond to this shift. The question is no longer "will this shift happen?", but rather "who will be the first to invest in it properly?" The opportunity is clear for those developers and investors who dare to read and respond to this shift.

References

Despite this clear shift in demand, real estate supply is lagging behind in keeping up with these changes. The Saudi real estate market has historically been designed to cater to extended or large families, with the average Saudi family size being 4.9 members.

From a purely investment perspective, the numbers prove that small units are the most viable in the current real estate landscape. In the first quarter of 2026, the average Gross Rental Yield in the Kingdom was 6.84%.

But when analyzing returns by unit type, studio apartments excel overwhelmingly. In Jeddah, for example, studio apartments in the Faisaliah neighborhood achieved a Gross Rental Yield of 10.4% in March 2026, outperforming larger units by 4 percentage points. In Riyadh, which recorded an average rental yield of 8.89%, smaller units continue to drive this growth driven by demand from young professionals and expatriates.

First: Low cost of entry: The cost of buying a studio is much lower than large apartments, allowing investors to diversify their portfolios and own multiple units rather than one large one.

Second: Higher rent per square meter: Tenants are willing to pay a higher value per square meter for a small unit in a prime location close to work and services.

Third: Low vacancy risk: A broad demand segment that includes young freelancers, professionals, students and expatriates ensures high occupancy rates throughout the year.

When it comes to single-family housing, a crucial segment that is reshaping the rental market in major cities cannot be overlooked: White-collar expats. A clear distinction must be made between laborers living in collective housing for workers and professionals seeking independent housing on the open market.

This influx of foreign talent, many of whom are between the ages of 30 and 55 and come alone at the start of their employment, is creating tremendous pressure on the small apartment and studio sector. Market reports confirm that residential rents in Riyadh have risen by more than 10% annually, prompting the government to institute a five-year rent freeze in the capital starting September 2025 to ensure market stability.

The phenomenon of single-family housing is not limited to Saudi Arabia, but is a rapidly accelerating global trend. But what distinguishes the Saudi case is the speed of transformation in a society that has traditionally relied on the extended family model.

Saudi Arabia stands today at the beginning of this wave. The lesson from international experiences is clear: Markets that were ahead of the curve and developed single-occupant housing products have realized exceptional returns, while those that lagged behind faced a surplus of large units and a severe shortage of small units.

The persistence of single-family housing will have a profound impact on the urban and economic landscape of the Kingdom, and three main axes of this impact can be identified.

The phenomenon of single-family housing is not just a passing trend, but a reflection of the demographic and economic maturity that Saudi society is experiencing under Vision 2030. Real estate developers who continue to build only ”extended family villas" may find themselves out of business in the coming years.

[1] General Authority for Statistics (GASTAT), Saudi Youth Statistics Report, 2024.

[2] Saudi Press Agency (SPA), "General Authority for Statistics Releases Saudi Family Statistics Report 2024".

[3] ASPAR Report No. 454, "Late Marriage Age in Saudi Society: Between Social Challenges and Economic Transformations," February 2026.

[4] ResearchGate, "Prevalence of Marriage Abstinence Among Saudi Youth".

[5] Ibid (Aspar Report No. 454).

[6] GeoFactBook/Ehsaeyat, Saudi Marriage and Divorce Statistics 2024-2026.

[7] Argaam, "Housing Statistics: 4.4 million housing units occupied by Saudi households in 2024."

[8] Bloomberg / Knight Frank, "Saudi needs to build 115,000 homes per year to meet demand," November 2024.

[9] Bayut, "Rental yields in Saudi Arabia: Top Cities and Property Types", Q1 2026.

[10] Sands of Wealth, "Rental Yield Data in Jeddah - The Studio", April 2026.

[11] Arab News, "Flexible sales models, pricing options drive Saudi households to homeownership apartments", March 2026.

[12] We Are Solo Living, "The Countries Where Solo Households Are Commonplace".

[13] Global Issues, "The Growth of One-Person Households", April 2025.

[14] Arab News, "Marriage, children and careers in Saudi Arabia".

[15] CBRE Saudi Arabia, "Saudi Arabia Real Estate Market Review Q4 2025".

[16] Global Property Guide, "Saudi Arabia Residential Property Market Analysis 2026".

[17] General Authority for Statistics (GASTAT), Labor Market Data Based on Administrative Records for Q1 2025.

[18] Arab News, Mercer report on housing and education allowances in Saudi Arabia, March 2026.

[19] Fragomen, Saudi Housing Market Report: Policies, Rents and Cost of Living, February 2026.